Tesla’s second quarter of 2024 (2Q24) has brought significant developments that are not only stirring the market but also setting the stage for what could be a transformative period for the company. This comprehensive overview will delve into the key aspects of Tesla’s recent performance, future prospects, and the broader implications for the electric vehicle (EV) and autonomous driving industries.

What’s the Story?

Q2 Sales Performance

Tesla’s Q2 sales figures have been a focal point of relief and optimism. With sales reaching 443,000 units, this marks a 14.8% increase quarter-over-quarter (QoQ) and a 4.8% decrease year-over-year (YoY). This performance slightly exceeded the consensus estimate of 439,000 units, as per Bloomberg, confirming that Q1 was indeed the bottom for Tesla’s sales. Notably, Tesla managed to reduce its inventory by producing 411,000 units, which is a 5.2% decline QoQ and a 14.4% decline YoY, thus reducing the surplus by 33,000 units.

Production Insights

Tesla’s production efforts in Q2 highlight several key trends. Despite a dip in overall production, the company has made significant strides with the Cybertruck, achieving an operation rate of 2,000 units per week. This momentum is expected to increase in the second half of the year with LG Energy Solution’s supply of 4680 batteries.

Financial Metrics and Consensus

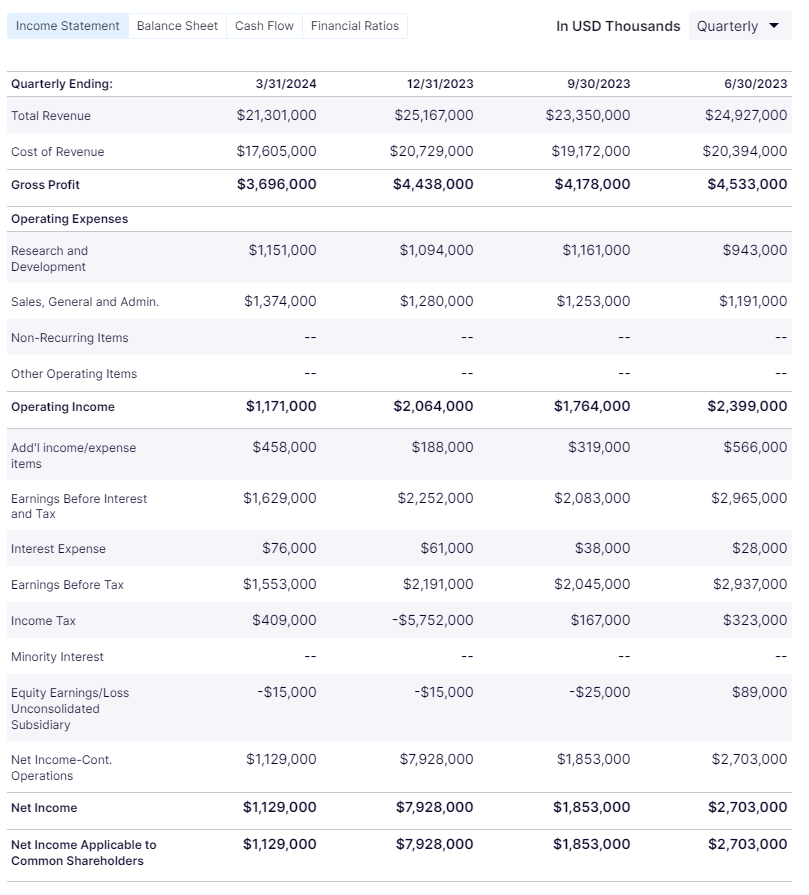

Bloomberg’s earnings consensus for Tesla in Q2 predicts sales of $24.13 billion, reflecting a 13.3% increase QoQ and a 3.2% decrease YoY. Operating profit is estimated at $1.84 billion, a significant 57.2% QoQ increase but a 31% decline YoY, resulting in an operating profit margin of 7.6%. Adjusted earnings per share (EPS) are expected to be $0.58, which is a 28.1% increase QoQ but a 36.3% decrease YoY.

Energy Business Expansion

One of the standout aspects of Tesla’s recent performance is the surge in Megapack installation volumes. The installation increased from 4GWh per quarter to 9GWh, driven by the expansion of Tesla’s US factory. This growth positions Tesla as a leader in the US energy storage system (ESS) market, with its energy business expected to comprise 12-13% of total sales in 2Q24. In 1Q24, the energy business recorded sales of $1.635 billion, a 13.7% QoQ and 6.9% YoY increase, with a gross profit margin (GPM) of 24.6%.

2Q24 Earnings Watch Points

Several key factors will be closely watched in Tesla’s 2Q24 earnings:

- FSD Subscription Rates in the US: The market will be keen to see how American consumers are reacting to and subscribing to Full Self-Driving (FSD) capabilities.

- FSD Distribution in China: There are high expectations for Tesla’s FSD technology in the Chinese market, especially given the recent regulatory approvals.

- Low-Cost Car Production and Model Y Facelift (F/L): Updates on the roadmap for low-cost vehicle production and the release schedule for the refreshed Model Y are anticipated.

- Cybertruck Production: Monitoring the production status of the Cybertruck will provide insights into Tesla’s manufacturing efficiencies and future output.

- Optimus Robot Development: Updates on the application and development of Tesla’s Optimus robot in factories will be of interest, particularly regarding automation and operational efficiencies.

Autonomous Driving and AI Aspirations

FSD 12.4 Supervised Version

Tesla’s advancements in autonomous driving technology are exemplified by the FSD 12.4 Supervised Version, which reportedly surpasses the average driving skills of American drivers. Despite this, it is not without its flaws, particularly in complex driving situations like unprotected left turns and intersection entries. The distribution of FSD 12.4.2 has been limited to employees and a select few, with mixed reviews comparing it to the earlier 12.3.6 version.

Economic Implications of FSD

From an economic perspective, the cost associated with FSD is largely a sunk cost for Tesla. All Tesla vehicles are equipped with autonomous driving hardware (Hardware 3.0 or 4.0), irrespective of whether customers opt for FSD. Despite the decline in profitability due to price reductions, FSD still boasts a gross profit margin of 66%, which is over three times higher than the EV business.

Transition to an AI Company

Tesla’s potential transition to an AI company is another critical narrative. The anticipated announcement of FSD licensing agreements or FSD implementation in China could act as a catalyst for Tesla’s recognition as an AI software entity. However, significant architectural changes are required for FSD to be integrated into vehicles from other manufacturers, which is expected to take approximately three years.

Valuation Considerations

Tesla’s valuation already reflects the market’s expectation of its evolution into an AI-centric company. The 12-month forward price-to-earnings (P/E) ratio stands at 86 times, which is significantly higher than other American big tech companies like Nvidia and Microsoft.

Chinese Market Dynamics

Sales Recovery

The Chinese electric vehicle market has been rebounding since the implementation of a new exchange policy in April. However, Tesla’s sales have remained relatively sluggish. While sales have shown month-over-month recovery with 62,000 units sold in April, 72,000 in May, and 71,000 in June, Q2 sales still fell short compared to Q1.

Interest-Free Installments

In an effort to boost sales, Tesla introduced interest-free installment plans in China after March. The down payment was reduced to 79,900 yuan, which is about 25-30% of the car price, with a maximum of five years for interest-free installments.

Autonomous Driving Tests

Tesla has made significant strides in the autonomous driving space in China. It became the first foreign company to receive permission for autonomous driving tests in certain areas of Shanghai. Tesla plans to obtain precise map software from Baidu by the end of the year, paving the way for potential commercialization of FSD and Robo-taxi services in China before the United States.

Government Procurement

Tesla’s inclusion in the Jiangsu provincial government’s list of new energy vehicle procurement is a significant milestone. The list, announced in June, includes 56 new energy vehicles, among which the Model Y is the only foreign brand. This inclusion underscores the growing acceptance and integration of Tesla vehicles in Chinese governmental operations.

A New Era for Tesla

The developments in 2Q24 signify a new era for Tesla, characterized by a delicate balance between current performance and future potential. The company has shown resilience in bouncing back from a challenging first quarter, with sales and production metrics providing a sense of relief and optimism. The surge in Megapack installations and the expansion of the energy business highlight Tesla’s strategic diversification beyond vehicles.

Moreover, Tesla’s advancements in autonomous driving technology and AI position it as a potential leader in these cutting-edge fields. The transition from an EV manufacturer to an AI-driven company is laden with challenges but also immense opportunities. As the market anticipates further developments in FSD and potential AI applications, Tesla’s valuation and strategic direction will continue to be closely scrutinized.

The Chinese market remains a critical battleground for Tesla, with interest-free installment plans and government procurement initiatives offering a path to recovery and growth. The approval for autonomous driving tests in Shanghai is a particularly promising development, indicating regulatory support and potential for early commercialization.

In summary, Tesla’s 2Q24 performance and strategic initiatives underscore the company’s ability to navigate complex market dynamics and innovate at the forefront of technology. The coming months will be crucial in determining how these efforts translate into sustained growth and market leadership, marking a new era for Tesla and its stakeholders.